Paying for war: Taxes versus debt

PSCI 2227: War and State Development

February 23, 2026

War increases tax revenue…

War increases tax revenue…

War increases tax revenue…

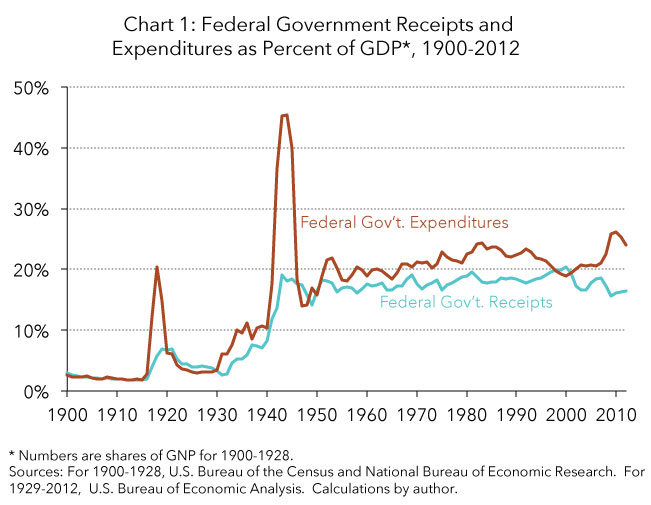

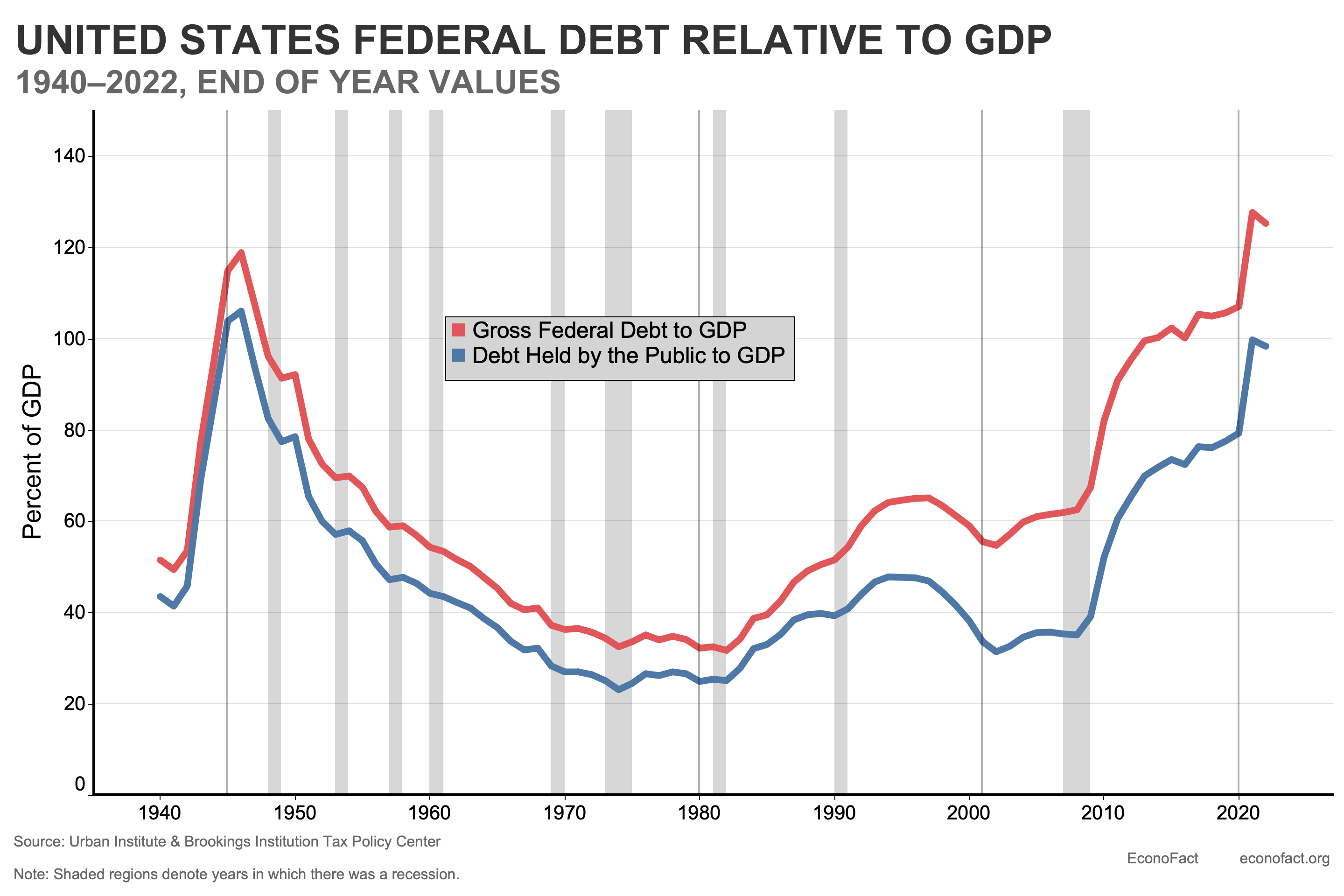

…and war increases debt

…and war increases debt

…and war increases debt

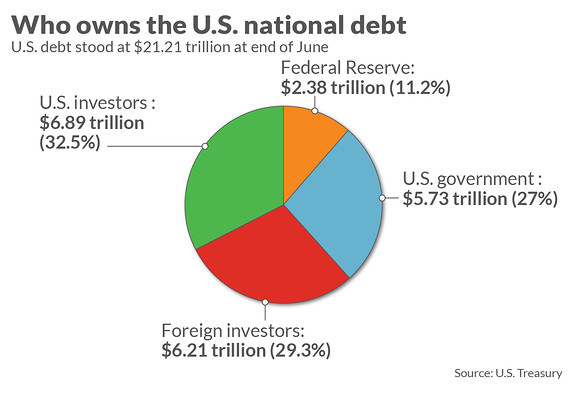

Who do states borrow from?

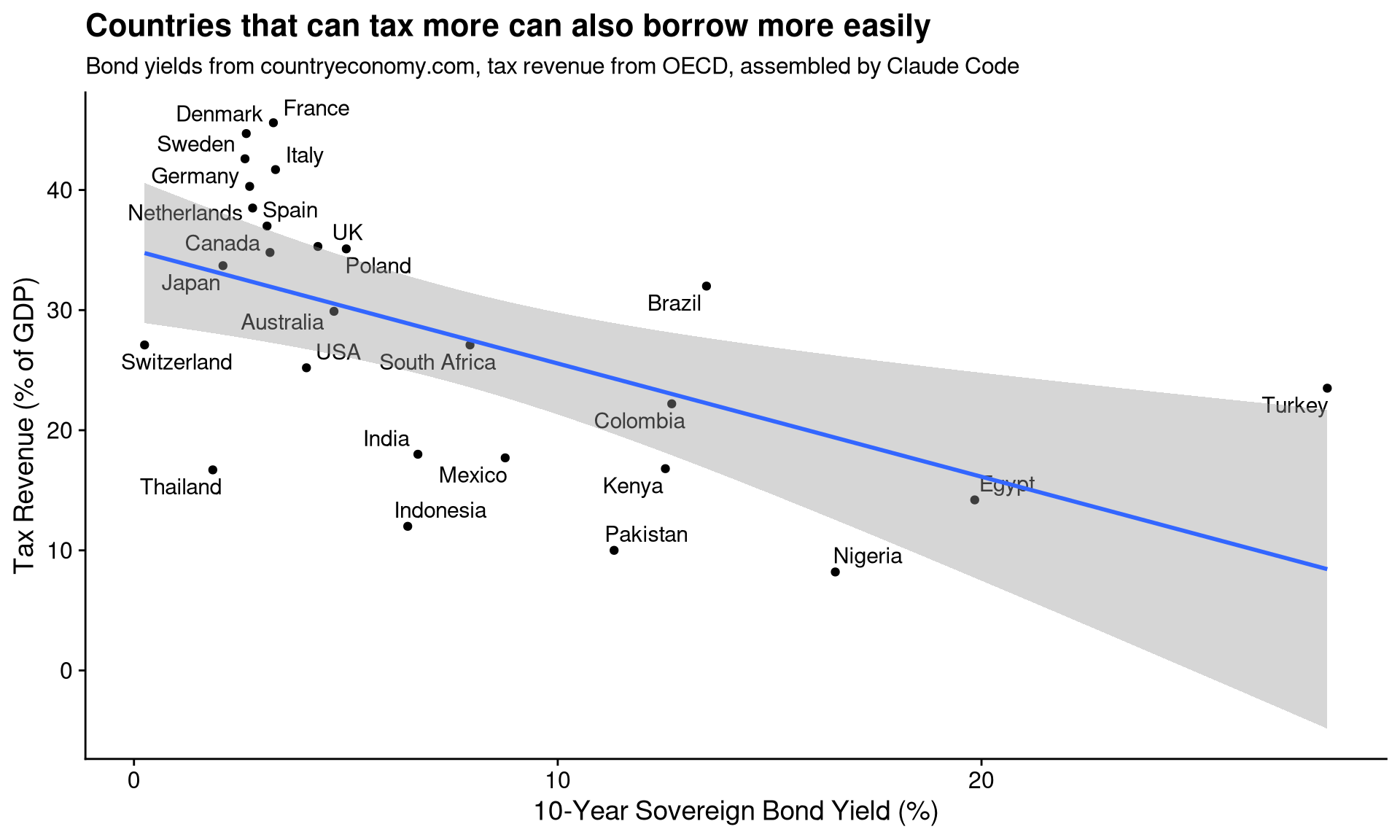

The endogeneity problem

Queralt’s solution

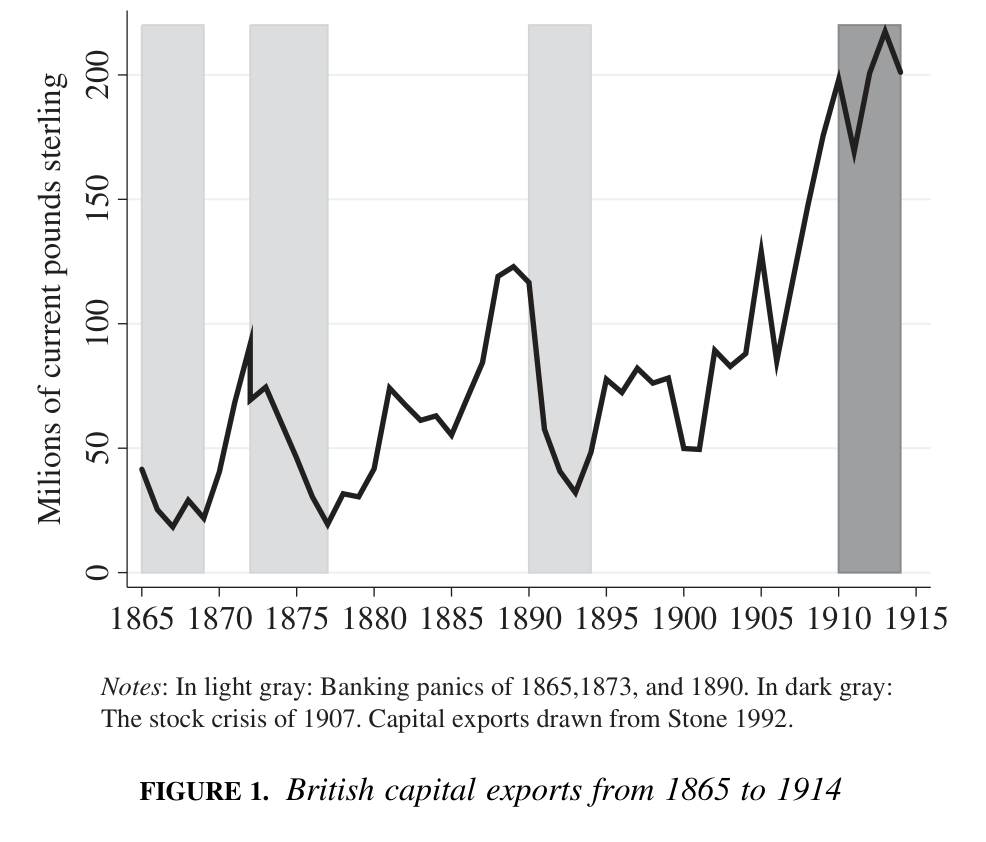

Britain was the “world’s banker” between Napoleonic Wars and WWI

Localized shocks to British markets \(\leadsto\) exogenous contraction of credit supply

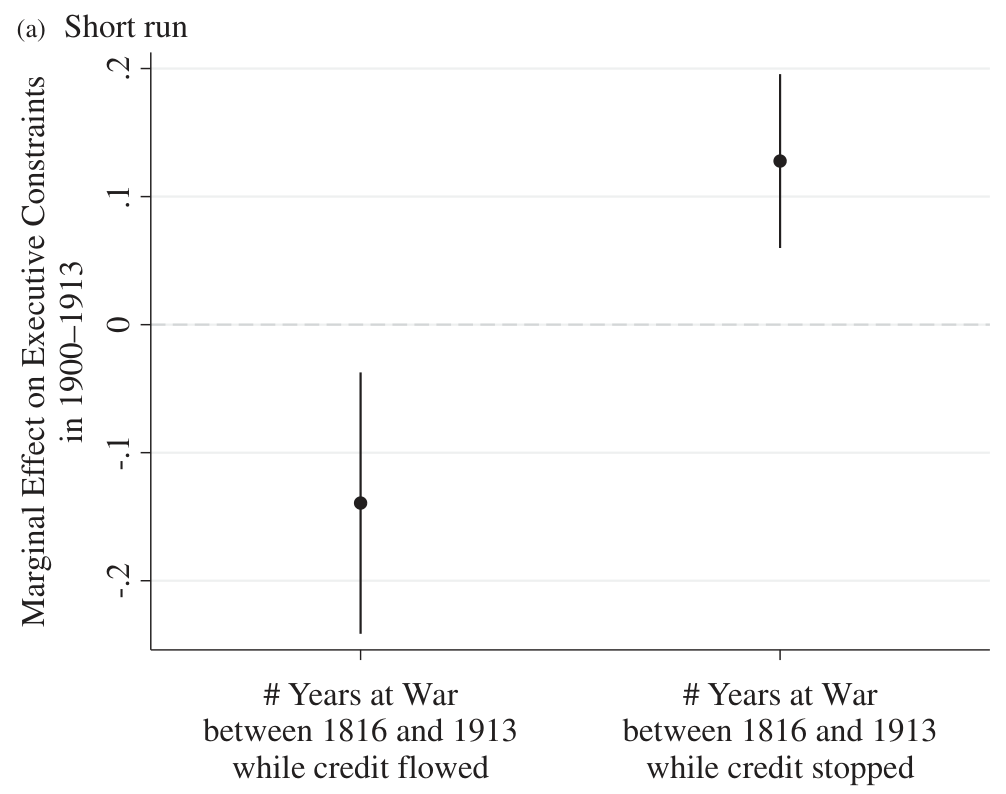

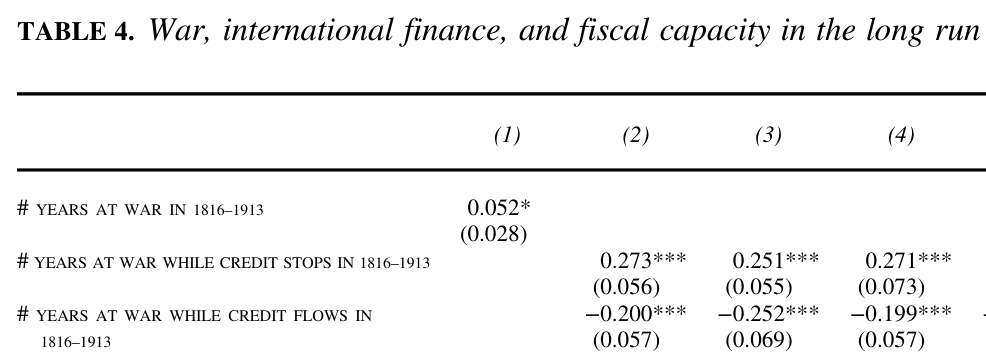

Statistical findings

Why does war-without-credit make the state?

Apparent mechanism: Forcing the ruler to share power